Global Banks: The Long View

With Q4 Earnings popping in I take a look at 20-Yr data to see where Global banks landed after their massive pre-crisis ambitions. As banks struggle to recalibrate, I try look at what potential areas of opportunity should look like. I also take a look at the Spectre of FinTech (which to paraphrase Jamie Dimon should have banks “scared shitless”), and dive into the unit economics thereof, courtesy Square and Ark Capital who have been most gracious with public disclosures

What a Winning Hand looks like

Looking at a sample of Global Banks, the last decade has largely been one of Revenue Stagnation. The most successful (JPM) can only boast a respectable but still humdrum 10-Yr CAGR of 2%.

What drove earlier growth pre-financial crisis? Looking at it from a product angle, one explanation is the massive amount of financial innovation in Pre-Crisis Era. These days, the alphabet soup of financial instruments is much sparser. If we takes SPACs out of the equation, a circa 2006 textbook would largely up to speed. Taking derivative notionals as a proxy for overall financialization, we can see exponential growth until 2008 followed by relative stagnation. It’s fair to say that the real drivers of value-add have pivoted towards technology and user experience.

Looking at historical business segment data some interesting observations pop up. The “Pivot to Asia” was a feature of many Banks’ growth Strategies. This doesn’t seem to have borne much fruit for local banks at least. ASEAN & Greater China revenues for SCB actually declined by ~5% over the 10 Year Period. BOA and GS fare similarly with both having better years during the earlier half of the decade. HSBC is marginally above 2012 levels but likely buoyed by cyclical FICC outperformances given the corresponding uptick in it’s “Global Markets” segment. Only JPM & CITI have a reasonable degree of Asia growth but the contribution to total franchise remains small. This is unsurprising as local banks in the same ten year period have grown phenomenally.

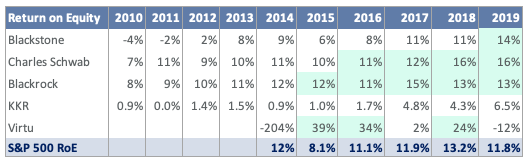

In terms of what’s worked, there are a few lessons. JPM and MS are two unqualified success stories both in terms of revenue growth and optimal returns. And RoE is really the guiding constraint here. Following stricter Basel Rules, stockholder capital at global banks has nearly doubled from Pre-Crisis levels. A detailed discussion of Basel is too complicated to get into, but in simple terms the riskier the asset the more capital one needs to cough up. So Credit Card lending tends to be more punitive versus say Mortgage Lending. As a consequence Fee and Commission based revenue streams are really the way to go if one is looking to optimize the business mix. While this includes I-banking, transactional revenues and potentially even FICC; a more definitive growth is to be found with equities execution, asset management, and even sales of non-proprietary Insurance & Investment products. Quite simply these are the areas where the overall wallet is expanding.

We can see MS following this route particularly in its recent acquisitions of E-Trade and Eaton Vance. MS is very much playing to its core strengths here being the global leader in equities. Comparables like Charles Schwab and Hi-Frequency Trading Firm VIRTU also tend to outperform the market on RoE.

This story is reinforced if we look at JPM’s business mix. One driver of its much vaunted RoE is the Asset & Wealth Management which boasts a 30% RoE. This makes intuitive sense as when a bank is merely investing “on behalf” of clients, the inherent risk and resulting capital requirements would be much lower. Even more striking is that the Consumer Bank also boosts an impressive ~30% RoE. And if you look at the revenue mix and compare it to say a CITI – what stands out is the relative contribution of Non-Interest Income (~30% for JPM vs 14% for CITI). While JPM doesn’t disclose investment sales numbers, its Consumer AUM is nearly twice that of Citi so it’s safe to say they have a superior fee-driven Investment Sales business.

For the rest of the Institutional side, the picture isn’t terribly exciting either. FICC Segment Revenues have been largely static. While the data isn’t publicly available FICC Wallet is generally believe to have stayed static in the last few years, and is one area where local banks have likely stolen some lunch. Investment banking & Corporate Lending are still growth but been outpaced considerably by Private Equity and Venture Capital. Indeed Dry Powder vastly outstrips public money, as is evident in data from Pitchbook.

Private equity firms unfortunately seems to be suffering from depressed returns similar to banks. Doing a quick sample check using a few Comparables, Equities (SCHWB, VIRTU) and Asset Management (Blackrock) really seem to be the way to go.

A Pivot towards the right capital-efficient businesses would be only bring banks up to curve. For the more interesting growth verticals, we should take a look what Fintech firms are trying to get at.

The Spectre of FinTech

FinTech has gone through a Cambrian explosion, and there is a lot of dry powder and public money out there dedicated to capturing the banking wallet. A lot of these business models, and even whole verticals (like P2P Lending) are not terribly interesting or a serious challenge. When the dust settles, its likely many of these firms will go the way of your neighborhood olive garden franchise. When Fintech firms do get it right, they more then knock the ball out of the Park. Recently listed Square already commands a market cap exceeding Goldman. Not bad for what essentially started out essentially as a merchant acquiring business (one of the unsexier and neglected units in a consumer bank). Buy-now-pay-later firm Affirm has a market cap of $28Bn, which is likely close to the value of Goldman’s entire Asia Franchise if you factor in GS’s 17x P/E Multiple. Given that there is nothing revolutionary about BNPL, the success of these firms really is a testament the uninventiveness of Banks’ distribution and Marketing strategies.

Working through the sheer number of Fintech firms and disruptive technologies is a problem. I tried breaking it down and visualizing the verticals in a common sense way. So let let’s try and look at it in terms of the whole payments cycle.

(1) You start off with money in your Pocket (or lack thereof)– and this is really the basic function of banks as a deposit taking entity. There isn’t really any drastic offering on the market. Platforms like AliPay, Venmo and Revolut have stolen some transactional deposits from Mainstream consumer banks it’s really a drop in the proverbial ocean.

One earth shattering development could be the eventual development of Central Bank Digital Currencies. If Blockchain succeeds in digitizing fiat currencies – individuals would be able to simply manager their own digital wallets without any need for intermediaries. CBDCs in my opinion, should inspire Sartrean levels of existential dread in the banking industry. While unlikely that regulators will allow widespread use of private wallets and eventual collapse of the banking system, we could potentially be looking at whole new models for banking in the very long run. China is really the bellwether here, with the pilot project for its digital yuan well underway. If any country has the ability to quickly push through a radical financial system changes, it’s China.

(2) On the Credit & Alternative Lending side, I believe Fintech has largely floundered. Fintech’s first real innovation was P2P lending side and we don’t really have any inspiring success stories. P2P Pioneer “The Lending Club” commands a market cap of less than a billion dollar (though SoFI is valued $8Bn by Private Investors). There are some interesting developments worth mentioning: (i) One is the development of behavioral data-based based credit decisioning. A good example is Ant Financial who leverage their Alibaba Customer history to score consumers (ii) Buy-now-pay-later has proven to be a lucrative market with AFFIRM leading this space with ~$28Bn Market Cap underscored by $10.7bn LTD Originations. Swedish BNPL start-up Klarna also commands a $10 Bn valuation in the Private Markets.

(3) As Mode / Medium of Payment – this is where I feel banks have majorly let themselves down. Even now few banks boast seamless payment apps like a Venmo, WePay or AliPay. Cross-border payments are an even sadder story, and firms like Transferwise have nicely filled this niche. Transactional revenues tend to be small, which is why I believe banks didn’t historically lead with technology investments. However, they failed to discern the potential for building ecosystems and distribution network around Payment Apps.

Instead of cultivating new distribution channels, banks relied largely on conventional Sales Forces strategies and traditional marketing and branding. strategic responses have also been defensive and short-sighted. When Apply Pay launched many banks didn’t sign up due fearing loss of interchange revenues and devised proprietary mobile pay alternatives. Of ecosystems, China’s Ant Financial is the leading success story perhaps, and Square in the US seems to be following suit with its twin Seller and Cash App ecosystems. Given the returns pressure - using a killer app as a segue to cross-sell fee based Investment products could have been just what the doctor ordered.

(4) Payment Gateways are essentially tools for Merchant to capture and validate credit card data e.g. POS machines or online checkout interfaces. And the merchant interface is something I feel banks neglected massively. PayPal, Square and Stripe have filled this niche out fantastically both online and offline. Apart from the blunt fee revenues, all three firms are building off their larger user Merchant user base Interface to cross-sell financial products.

(5) Payment Processors are the plumbing of the whole financial industry. And this consists of byzantine clearing organizations and companies like MasterCard and Visa. Antiquated payment processors are what make cross-border payments so complicated. Apps like TransferWise who simplify this process have gained a significant following. FinTech solutions in this area, however, are likely to be centered on helping Banks rather thanks supplanting them. So it’s largely been a mixed bag (see: Ripple)

(6) Coming back to the end of the Payment Flow. You’ve got your money and have to do something with it. While all banks boast e-brokerage services or digital investment services, they User Interfaces highly unintuitive or outright cumbersome. And Robinhood is a great success story here which has spawned an entire subcultures of dedicated retail investors (Private Markets value it at $12 Bn) is a case in point. Another Vertical dedicated to smoothing out these issues are the so-called “Neobanks”. These are usually mobile-only or digital-focused banks who try to provide transparency and take the complexity out of banking. Unfortunately, these have largely struggled to take off. Monzo and N26 are some high profile failures. There are some notable local champions though. Brazil-based NuBank boasts a substantial customer base of ~20mm. One of the more interesting case is SBER, the largest Russian bank which is essentially a Deliveroo, an Uber, and a bank all rolled up in one (made possible to a degree by Russia’s regulatory environment). What’s interesting to note is SBER boasts RoE ratios in the high teens, and IMO validates the need for diversified fee-based revenue streams.

The Prize

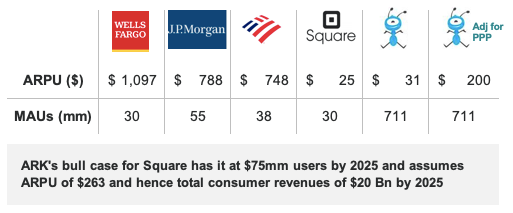

To size up the potential opportunity from Fintech, we’re going to take a deep-dive into unit economics. The valuations of Fintech companies are really predicated on their ability to ultimately monetize their massive user bases. ARK Invest has recently articulated a bull case for Square where SQ scales up its monetization efforts. Effectively, the bull case it works out to SQ upping it’s Cash App revenues from $530mm in 2019 to ~$20bn in Revenues by 2025. While wildly optimistic, tinkering with the ARPUs and potential user base here, gives one a sense of the vast prospects involved.

The growth in MAU and digital users for Fintech firms has been nothing short of extraordinary and there is more than enough room for user growth in the US as the China example of AliPay shows (WeChat’s MAUs are even more impressive at ~1.3Bn). Digital MAUs at US banks are not all bad at all and even though growth trends are fairly anemic; the ARPUs are off the charts.

The average US bank has an ARPU of ~$880. ARK assumes Square would be able to land at an ARPU of $280 by 2025 by expanding their product offerings. The forecast also assumes a doubling of its user base from 30mm to 75mm. The math works out to (75mm * 280 ) ~$20bn of Consumer Revenues off the whole “Cash App” ecosystem.

And this is really a scenario where Square’s Cash App is diligently used by 1 in 4.5 Americans for multiple banking needs. We don’t have any precedent for comprehensive ecosystem in the US. Taking Ant Financial and crudely adjusting it for Purchasing Power Parity (times USD/RMB) we land at $200 ARPU.

ARK’s assumptions are quite loaded here but some other markets have ultimately converged towards a dominant killer app. It’s possible that US remains fragmented with the status quo holding. Nonetheless, this is an interesting scenario which gives a sense of the endgame for FinTech and where banks should probably be headed.