Meituan: China Tech Series #2

A look into the origins of the "SuperApp of Services"

Welcome to The Macro Geek, where I write on themes in business, finance and technology. If you haven’t already done so already please hit subscribe 📨

Hey Folks 👋

Earlier, I wrote a piece titled “China Tech vs. the World”. As I’ve come up the curve on the subject, I’ve decided to do a series of follow-on articles which probe China’s tech giants further. In this article, I look at Meituan. While deep-dives, these will largely be exploratory pieces rather than full-blown investment theses

Meituan is China’s third largest tech company behind only Tencent and Alibaba (and fifth largest overall) by market cap. It’s frequently described as a combination of Doordash and Airbnb. And while that’s largely true, that narrative sort of undercuts Meituan’s larger remit. I would position them as the SuperApp of Services; they are the leader in Offline to Online (O2O), and the Meituan App can basically serve up anything from a haircuts to dental cleaning. The rise of SuperApps is a theme that looms large in the tech world, and I would say Meituan has possibly the strongest claim to being one.

Their roster of services is actually ridiculously impressive. And booting up the app is quite the sensory experience. It’s core services are Food Delivery (being China's deliveroo / doordash equivalent), Hotels & Accommodation (being China’s Airbnb and booking.com equivalent) and of late Community Group Buying (if you’re unfamiliar with group-buying check out rival Pinduoduo’s explanation – slide 4 is pretty self-explanatory; or my own PDD article).

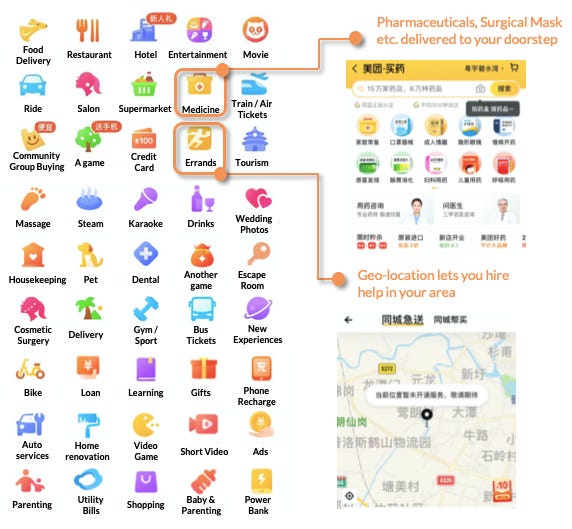

This is the home screen, and you can actually flip here through 3 pages worth of services

I’ve overlaid the full roster below, and it comes to a whooping 45 icons (!). You have a restaurant directory (replete with discount coupons), bike-sharing, ride-hailing, delivery of medical supplies, movie tickets, hired help (plumber, mechanic etc.), train and air ticket booking and even “escape rooms” (more here on this ridiculous trend).

So what how did Meituan get to where it’s at? It actually started out life as a Groupon clone. Most Chinese tech firms did in fact start off as regional knock-offs, but as an exasperated former US President would tell you, they are quite formidable now. It’s a point I’ve belabored in earlier posts, but China tech seems to have displayed superior commercial acumen in refining their business models. The original Groupon is a bit-player now, whereas Meituan is one of the most valuable tech companies at this point. And Meituan founder Wang Xing’s story is very much emblematic of this trajectory.

Wang Xing: The OG 40 under 40

In 2018 Fortune ranked Wang Xing 3rd on its 40 under 40 list, second to Lyft founders Logan Green and John Zimmer. It’s a curious choice, as Lyft now has a market cap of of ~17Bn while Meituan is closer of $220 Bn. A Tsinghua graduate, he cut his teeth creating clones and rip-offs of western tech companies, and during his earlier career was literally the personification of copycat China. His first successful venture was “Xiaonei”, a Facebook-clone. A cash-strapped Xing eventually sold off this venture but it survives to this day as “RenRen” a declining (but briefly successful) social network. He then dedicated his efforts to “Fanfou”, a Twitter clone, which was eventually eclipsed by Sina Weibo and other players. Meituan was Xing’s third venture and while initially more modest in scope (being a mere Groupon knock-off) it finally emerged as something far more daunting and original thanks to his resilience and execution.

Wang had initially dithered between opening a Groupon clone or a Foursquare clone, before settling on the Groupon model. Meituan spent its early years aggressively building a merchant network (as of 2020, the company counted a staggering 6.8 Mn merchants on its platform). China’s consumer market was cost-conscious and deal-savvy, and a Groupon-like platform grew well. Meituan even took on the OG Groupon’s Chinese affiliate “Gaopeng” and won largely thanks to aggressive merchant pricing. Gradually they started expanded their offerings to airline tickets, movie tickets among other items. In 2013 they made the fateful decision to enter Food Delivery.

In 2016 - Wang Xing inaugurated the beginning of the company’s “second-half”; having secured a decent user and merchant base this phase which would be driven by the deepening of the ecosystem. And this is whereas where we see the beginning of its awe-inspiring revenue growth.

Meituan’s Numbers

Food delivery has remained the strongest moat for Meituan particularly during the Pandemic and has offset some of the (also Covid-induced) stagnation in its other segments such as travel. Food Delivery’s FY2020 Gross Transaction Value for its food was a staggering ~$75bn compared to Doordash’s $20Bn. They are also the dominant player in the Travel segment having eclipsed rival Trip.com. And given it’s reliance on domestic tourism you don’t see as drastic a drop in post-pandemic 2020.

Profitability is very much in the red, however. The firm stopped breaking out gross margin by segment a few quarters ago and it’s difficult to tell what the real value of Meituan’s product lines is excluding Marketing and Sales costs. This is a wider problem with assessing sharing economy and platform service firms, as margins often tend to be razor thin on key offerings like ride hailing and food delivery. The ultimate hope is to pivot into more value-added areas and Meituan does seem to have at least one big one with it’s “In-store, hotel and travel” segment delivering a ~$1.2 Bn operating profit. This is more than offset by it’s “New Initiatives” losses where the firm adopts a bleed-to-grow approach.

The company has explicitly stated that it will be in the red for several quarters as they continue to expand aggressively. The focus very much looks to be on expanding Community Group Buying and targeting lower Tier Cities per Wang Xing in the last earnings call.

And we are very committed to continue investing in scaling up our community e-commerce business. Through our efforts to build-out our supply chain and next-day delivery capability, this business model provides broader SKU selections with much more convenient shopping experience and lower price, in turn allow us to acquire a vast new user base and less accessible and rural areas.

And in another echo of Pinduoduo, there is a focus on fostering a direct consumer-to-manufacturer (C2M) relationship for . PDD has some investor slides on the topic which are great academic reads.

During the quarter, through the cooperation with some local governments, we launched the Agricultural Produce Direct Sourcing, [Foreign Language], that program in some pilot areas such as Yunnan, Jilin, and Guangxi province to reduce intermediary costs, improve our supply chain efficiency, accelerate [indiscernible] infrastructure development, help farmers generate additional revenues and lower prices for consumers.

Meituan’s transacting users stand at 510mm - not quite at Alibaba’s level but significant enough to poke the giant. Alibaba has been pivoting from an online-only platform to O2O services as well. This is a key pivot for Alibaba and it has recently formed a life services division to compete with Meituan in this space. However, Meituan has been on the ground for years and this history has paid off. Alibaba’s food delivery effort Ele.me plays second fiddle to Meituan.

Alibaba was actually an early investor in Meituan having led its series C Funding. However, it backed out in 2016 choosing to allocate capital to its own O2O effort Koubei - an effort that hasn’t born as much fruit. Tencent has since backed Meituan though and owns around a fifth of the company.

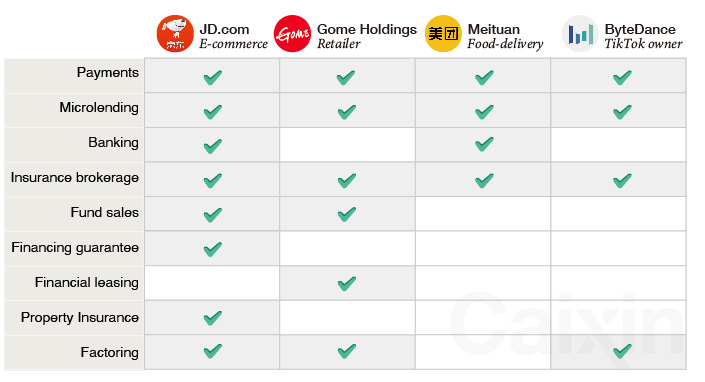

Meituan’s infrastructure building efforts during it’s pre-takeoff years are one reason it remains so resilient. One landmark acquisition in 2016 of local payments operator Qiandai pay, which endowed Meituan with Payments and Microlending license. Meituan users can easily access some ready credit and defer their purchase payments by a month. Meituan has also launched its solo payments Meituan and co-sponsor credit cards (these efforts are admittedly less bedazzingly successful).

It continues to invest in physical infrastructure as well. It has also rolled out an autonomous last-mile delivery vehicle reminiscent of those employed by Alibaba’s Cainaio.

Of SuperApps and greater Monetization

The key trend Meituan exemplifies and the one I’ve been building up to is platform consolidation and the inevitable rise of SuperApps.

Sharing economy pioneer Uber has attempted the same perhaps too little and too late. It shuttered its foray into payments and digital wallets and also shuttered some Uber Eats operations as well. The new verticals it’s focused on include grocery and consumer products, which are areas Chinese players like Meituan and Pinduoduo have already mastered.

Uber really is an exemplary case example here. I do think think the pendulum has swung wildly at Uber, from an impetuously aggressive team to a relatively by-the-numbers uninspiring team. Emil Michael, Uber’s former Chief Business Officer and Korean brothel connoisseur, had this much to say on a recent Bloomberg interview.

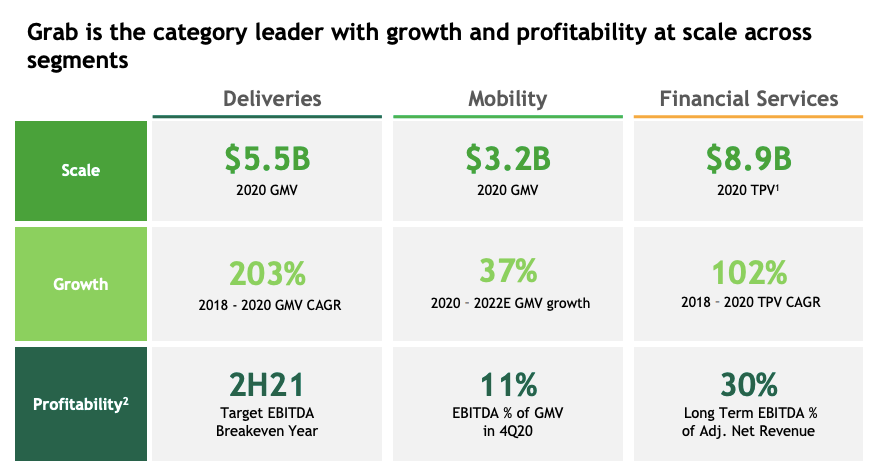

Meituan’s South-east Asia rivals, Grab and Gojek exemplify this approach just as well and Grab’s recent investor deck shows it leveraging this strategy to great effect and also succeeding in the relatively difficult Payments space.

Another interesting slide from Grab shows their strategy of integrating themselves into consumers lives. This is a striking representation of the endgame for Chinese Superapps like Meituan and Wechat. Synergies aside, just the Big Data aggregation benefits should be quite phenomenal.

I believe SuperApps are a long-term inevitability and it’s a topic I find extremely fascinating. You have many use-cases emerging around the world particularly across Asia. All of these have taken different paths to capturing their user bases, and have achieving profitability. Now that a lot of investor disclosures are available, I’m compiling the data to look at the trajectory and economics thereof, and I believe there may be a few theses to be mined about which verticals are more valuable. Stay tuned!

That’s all I have for now. Thanks for reading 🙏