The Chip Industry: Origins, Key Players and Geopolitics 📱

Or why semiconductors are the new "oil"

The Semiconductor Industry is one of the most important strategic flashpoints in the world. With supply chain shortages, US-China tensions, computer chips are becoming the new “Oil”. Moreover, the world is set for a momentous infrastructure overhaul with the onset of technologies like 5G, IoT and Autonomous driving; the hardware behind all this will be powered by a handful of companies. Semiconductors are also crucial to critical military technologies as well. To take an example, Lockheed Martin’s F35 fighter jet uses computer chips sourced from Taiwan’s TSMC – who’s foundries are barely 100 miles off the coast of China. It’s likely that other sophisticated military hardware like the Predator drone rely on foreign foundries as well. And this explains why Chip self-sufficiency has become a pressing policy issue for the US with Biden earmarking $50Bn to boost the American chip industry.

In spite of all this, the Semiconductor industry has been relatively ill-covered until recently. When I started reading up on it I could hardly find any condensed and accessible overviews. It’s perhaps due its back-end, unglamorous nature that the industry and it’s luminaries have been only infrequently discussed in popular discourse. TSMC’s founder Morris Chang is certainly more influential than household names like Tim Cook; but he rarely receives a mention in our pop culture pantheon of business leaders.

In this post, I’m going to try and cover the key players, the birth of the industry, and the people behind it. I will try to explain the supply chain as best as I can, with the help of tear-downs of the iPhone 12 and Galaxy S20. Finally I’ll try and give some overview of the Chinese players active in the semiconductor space that could potentially challenge their global counterparts in the coming years. Before kicking it off, special hat tip to Jon’s fantastic Asianometry channel 🎩. I’ve been following it for a couple of years and it is quite frankly largely responsible for my semiconductor education.

A good starting point is the Foundry-Fabless distinction; and this is basically the Rosetta stone to understanding the history and structure of the semiconductor industry. Prior to the “foundry model”, the entire chip production process was managed end to end in-house by one company. Nowadays, Intel & Samsung are the only companies still somewhat trudging along this route. Most companies though have gone “fabless” and outsourced production (or “fabrication”) to companies like TSMC. So you essentially have “design” companies like Qualcomm & NVIDIA who basically build the IP for chips and outsource production to a foundry like Taiwan’s TSMC. So we can break up the process as follows:

There are some other critical players along the way – most important of which is Advanced Risk Machines or “ARM”. ARM provides one of the most critical IPs – the instruction set or architecture underlying chip design. ARM pretty much has a monopoly on mobile chip instruction set and most semiconductor companies depend on it. Another critical supplier is Dutch firm ASML which is the only firm in the world manufacturing critical photolithographic machines essential to the chip manufacturing process.

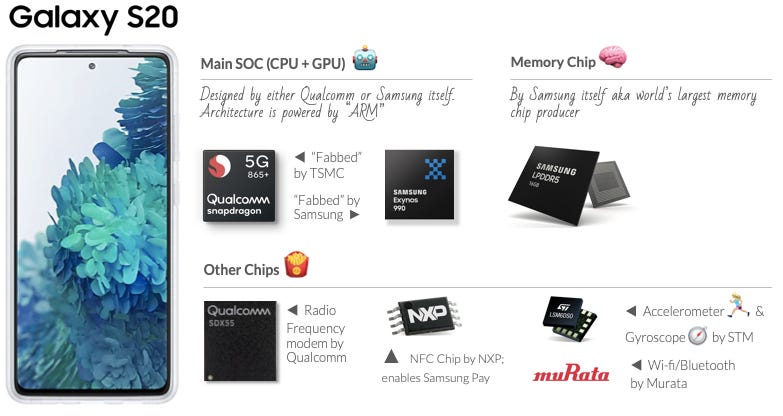

To understand this better intuitively, let’s try and do a simple teardown of the Samsung Galaxy S20. The details are sourced from the folk over at iFixit here; and please excuse any unintentional errors as I am basically a non-technical person doing this as a one-off. I do another for the iPhone 12 at the end as a way of recapping it all up.

We have the key Chip being designed either by Qualcomm or Samsung. Galaxy S20s released in Korea contain Samsung’s own “Exynos” chip which it both designs and manufactures. Phones sold internationally make use of Qualcomm’s famous Snapdragon 865. The Snapdragon is designed by Qualcomm but manufactured by TSMC. On the memory, Samsung itself manufactures the memory chip – no surprise as it is one of the biggest memory chip players as we will see later too. As you can see in the iFixit link above, the phone contains a plethora of other chips, but I’ll just go through a few of these. The Radio Frequency receiver is again provided by Qualcomm. The Near-Field Chip which lets you wave your phone to enable payments is provided by NXP (a Dutch ~$9Bn Revenue which dominates Near Field tech ). The Accelerometer and Gyroscope chips come courtesy of European Manufacturer STMicrolectronics. whereas the WiFI & Bluetooth chips are provided by a little-known Japanese company called Murata. As you can see from the original iFixit article, the phone contains a lot more in terms of semiconductors, and the ones called out are just to give a sense of the complexity involved.

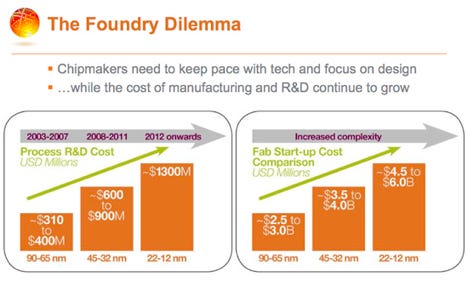

Now we can take a look at the companies in more detail. As mentioned earlier, the Foundry-Fabless distinction is important to our story. When the semiconductor industry first started out, the entire process from design to fabrication was managed in-house. The cost of building a foundry is quite prohibitive, however, and foundries also tend to get outdated pretty soon. TSMC’s latest cutting-edge 3nm foundry been estimated to cost ~$20bn. Coupled with massive R&D costs, it makes sense to outsource and industrialize production. Foundries like TSMC can cater to multiple designers and benefit from economies of scale.

AMD was one of the last holdouts here. It’s founder famously proclaimed “Real men have Fabs”; a dictum that did not age well - it divested its foundry business to Mubadala, Abu Dhabi’s sovereign wealth fund in 2008. A slide from one of their earlier investor decks at the time captures the dilemma nicely. Integrated chipmakers are forced to juggle rising R&D costs along with Fab start-up costs.

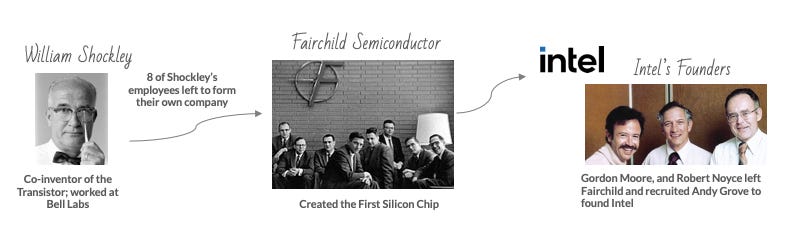

As of present day, we have two players who stick to owning their own foundries. One of these is Intel. Intel of course has a storied history and was to a great deal responsible for the birth of the modern chip industry. The Semiconductor transistor was first developed at Bell Labs by a certain William Shockley. Though he and his cohort would go on to win the Nobel Prize, he himself was a bad boss, and eight of his employees (famously known as the “traitorous eight”) left to form their own venture called “Fairchild Semiconductor”. Although now defunct and largely forgotten, Fairchild is one of the most consequential companies in human history.

They developed the first Silicon chip and kickstarted the growth of what would eventually be known as Silicon Valley. “Intel” was similarly born of another exodus when Gordon Moore (of “Moore’s law” fame) and Robert Noyce (who proposed Silicon be used as a chip material) recruited Andy Grove and left Fairchild to form their own company.

Intel created the first commercially available microprocessor. Though still a formidable company, its relative decline is emblematic of America’s current standing. It’s market cap of $225Bn is less than half of TSMC. Technologically, its foundry business is also behind TSMC only being capable of manufacturing chips with a 10 nanometer density where TSMC is moving towards 3nm. In the traditional PC market, it’s losing market share to AMD’s Ryzen, and their dynamic CEO Lisa Su.

Over the years, they also resisted moving into the mobile market instead sticking to the computing market which it knows best. One reason for is its adherence to the x86 Architecture. We mentioned earlier that one of the core IP for making a chip is an “Instruction Set Architecture” (ISA) which basically defines the fundamental operations of any chip. If you’re a semiconductor designer, there are really two options for licensing ISA IP in the market – x86 powered by Intel for computers, and ARM’s architecture which is more suited for mobile devices. This strategy does give Intel a good moat, but even here it is losing ground to ARM as Apple recently opted for ARM to power the chips in their Macbook.

There are many views on what Intel could have done. It’s insistence on maintaining the Foundry business have been questioned by many. In spite of this, it only seems to be doubling down on the Fab game with a recently announced $20Bn a new “IDM 2.0” Fab Strategy. Reaction has been mixed but timing wise this does coincide with the US’s stated intent to pursue semiconductor self-sufficiency.

The other “Integrated” player is Samsung. But Samsung operates it’s foundry closer to a pureplay model, where it not only powers its own chips but accepts orders from other designers like Qualcomm, NVIDIA ala TSMC. And this is actually what Intel is now pursuing with its recently announced 2.0 Strategy”. It’s also worth noting that Samsung’s foundry boasts a 5nm process - more advanced than intel and second only to TSMC.

The Foundry business is of course synonymous with TSMC. And the birth of TSMC is very much intertwined with Taiwan’s emergence as an “Asian Tiger”. It’s a fantastic triumph of industrial policy and state planning, which many countries have tried to replicate to no avail.

TSMC was” incubated” so to speak by the state sponsored Industrial Technology Research Institute (ITRI). The ITRI was a government agency explicitly tasked with uplifting specific sectors for economic development. Taiwan’s economic minister (and eventual premier) through much of the 60s and 70s was the highly capable Sun Yun-Suan. He is widely credited with pushing Taiwan to upgrading it’s technology. The policy choice to focus on Semiconductors is credited to a Chinese-American engineer named Pan Wenyuan.

The ITRI’s first semiconductor company was United Microelectronics (still around under the twin firms of UMC and Mediatek). The creation of TSMC soon followed as a foray into more advanced VLSI (very large scale integration) technology. It’s founder Dr Morris Chang is a beloved hero. He spent most his career in the US at Texas Instruments where despite a fast track career, he was ultimately sidelined. He was already 52 by the time he quit Texas Instruments and started working with the Taiwan government. And it’s quite remarkable that at an age where most careers are already drawing to a close, his main act had had only begun. He continued to steer the company till his retirement at the age of 86 (!) in 2018.

TSMC is likely the most strategically important company in the world right now. It is the most valuable semiconductor company by market cap, and it’s revenues are approximately 6.5% of Taiwan’s GDP underscoring its importance as a national champion.

Other Players

In this section, I want to take a dive into more of the companies involved in the chip-making process. We’ve talked a bit about ARM, TSMC, Intel and Samsung but other players are just as consequential. We start with the Fabless chips designers:

Qualcomm: We referenced Qualcomm earlier as the maker of the Snapdragon Chip used in the Galaxy S20. This is perhaps its most famous product and is used across Xiaomi, ZTE, Oppo and LG phones as well. It also owns a substantial cache of IP and actually earns around 70% of its EBIT from licensing fees. Qualcomm was the subject of a hostile takeover by Broadcom a few years ago, and a proposed merger was blocked by Donald Trump on national security grounds. The underlying cause seems to have been the fear of the US losing a national champion, and ultimately its edge in making chips.

Broadcom: Broadcom focuses on networking and connectivity. Their chips are used in Cell Towers, Data Centers, and Fiber Optics. Broadcom claims 99.9% percent of internet traffic has passes through at least one of their internet chips. On the more obvious consumer end, they are big supplier of wireless components for phones. Iterations of the iPhone have used their WIFI chips, Bluetooth chips, as well as well as the Radio-Frequency chips that enable a phone to connect to cellular data. Apple is indeed a huge customer, and Broadcom was mulling the sale of its Radio Frequency Division until striking a large multi-year contract with Apple. Apple accounts for approximately 20% of their revenues

NVIDIA: NVIDIA’s recent rise is a well-covered story so I won’t get into much detail. Suffice it to say that the GPU / Gaming business is their main driver, which also powers the crypto mining infrastructure. Their “Data Center” segment which provides high performance chips to AWS, Azure and other cloud providers is catching on real fast, and may just eclipse gaming GPU revenues.

Next to TSMC, Nvidia is the second-most valuable semiconductor company. It is by far the most valuable American semiconductor company with its valuation a multiple of American mainstays Intel and AMD.

MediaTek: MediaTek is a Taiwanese fabless originally spun off from their first semiconductor company UMC. Their “Dimensity” SOC is widely used in mid-range phones. They also power TVs, tablets and routers and claim to be in 1 in 5 homes.

On the foundry side of things TSMC and Samsung really dominate (collective 74% market share), but rounding up the top-5 are GlobalFoundries (formerly AMD’s foundry biz), UMC (Taiwan’s first attempt at a semiconductor company and TSMC’s older step-brother) and China’s would-be national champion SMIC (more on that later).

Another significant semiconductor segment is memory chips (FLASH, NAND, DRAM etc.) which is dominated by Samsung’s Memory division, another Korean company SK Hynix and US-based Micron.

Rounding out our discussion are companies operating on the deep back end. We have to mention ASML – who are responsible for manufacturing this ginormous photolithography machine essential to the semiconductor fabrication process. Critically, they are the only supplier of this machine (a friendly Reddit user pointed out that Nikon also operates in the space though at a substantially smaller scale). One way the US is forcing China’s hand is disallowing ASML (a Dutch company) from selling to Chinese chipmakers.

Cadence and Synopsys are also worth a mention as they provide “Electronic Design Automation” software similarly critical to designers like Qualcomm.

As a recap, we do a simple teardown of the iPhone 12. Once again the details come from the fine folk at iFixit. What’s different here is that Apple design’s its own chips unlike other mobile phone manufacturers. So we saw the Galaxy S20 being power by Qualcomm’s snapdragon in some markets, but Apple is the designer in lieu of Qualcomm here with TSMC once again doing the honors for Fab responsibilities. On the memory front, it’s a mixed bag with some phones boasting Micron chips and others using SK Hynix.

For the rest of the chips the configuration is quite similar with Qualcomm footing RF and NXP and STM rounding out the next. I couldn’t find details on WiFI/Bluetooth chips but it’s likely Broadcom doing the deed.

China Rising

In the final section I want to take a quick look at how China is catching up. While this is much talked about in the press; there is very scant coverage of the actual players driving it. One reason may be that many of these Chinese firms are relatively behind. The imperative for China to achieve self-sufficiency can be captured in the following graph. Semiconductors are by a large margin China’s largest import eclipsing even oil.

Two Chinese companies that had a definite chance (and may yet still) of becoming global champions were HiSilicon and SMIC. HiSilicon is basically the chip design arm of Huawei – and has since been hobbled by US sanctions. It may have to discontinue its relatively sophisticated “Kirin” mobile chipset on account of the potential double-whammy of losing access to ARM technology, and use of TSMC’s foundries.

SMIC is china’s leading foundry and the world’s fifth largest by market share. It stands a few generations behind the likes of TSMC and Samsung though with SMIC only having a 14 nanometer process. SMIC is similarly at risk of being cut-off from critical technology by way of losing access to ASML’s photolithography machine.

In terms of the present landscape – we have quite a few players. It’s worth noting that nearly all of these are operating on the lower end of the spectrum in terms of technology. The below list is my own curation and not comprehensive.

Many Chinese semiconductor firms operate in the white label space, and Allwinner and Rockchip are good examples of fabless designers who effectively cater to the cheap tablet market. We do have some promising local champions working on more advanced AI chips – and I’ve mentioned Verisilicon and Cambricon as representatives thought they are still nascent companies. China’s other large design company “UNISOC” is potentially threatened by the bond default of it’s parent group Tsinghua Unigroup. On the memory front, Yangtze Memory Technologies and GigaDevice are notable mentions. This space will continue to evolve; China boasts two semiconductor state funds colloquially named “Big Fund” and “Large Fund” and they will have a role to play in selecting and calibrating national champions.