The "Plumbing" behind Payments 🔩

The "Plumbing" behind Payments 🔩

And the Future of Money

In this article, I dive into obscure rabbit hole of the world of Payments. An ill-understood area, the “plumbing” behind payments is the Rosetta stone to understanding both the legacy and the future of finance. We’ll cover cross-border, domestic payments, credit card networks and blockchain-fueled next generation developments.

Right now, the Payments field is now one of finance’s most contested battlegrounds. But little more than a decade ago, this was one of the unsexiest areas for aspiring finance professionals. Now firms like Square, Stripe, and Alibaba to name a few, have built payment-centered ecosystems and boast of valuations exceeding many universal banks. To a degree, this is a story of institutional and regulatory neglect. On their own payments aren’t the most lucrative business, which is why they have been something of an afterthought for banks. But the potential of leveraging payments to capture a user base and then subsequently monetizing it through cross-sell was something tech firms better foresaw.

With rising nationalism, payment systems are also becoming a political tool. The US wields the stick of revoking access to USD Clearing system. Many Russian institutions were cut off from USD clearing following the Crimean annexation. In the event of further US-China escalation, this may once again come into play. CBDCs are another contentious space, with China kicking off (and leading) a latter-day space race.

To understand all these developments, and put them into context I’m going to try to sketch a complete taxonomy systems and analyze at the “plumbing”. As we’ll see, a lot of the complexity around is due to the sheer number of systems, many of which are just layered on. Take the case of the case of US’s key payment systems. For domestic payments you have the veritable alphabet soup of Fedwire, CHIPs, ACH, NYCE, STAR, and the TCH’s RTP. And this is in addition to Visa, Mastercard, Amex, Discover, and the cheque clearing system. A lot of these also fairly archaic; The Clearing House’s Real Time Payments System was only implemented in 2018 and was the United States’ first new payment system in 40 years!

National Payment Systems

We’ll start off by taking a look at the state of national infrastructure. These days, many advanced countries have rolled out infrastructure capable of real-time payments. These are networks which enable 24x7x365 instant delivery, and are payment systems fit for the digital age. So if you use your banking app to transfer funds to your buddy; it’s back by an RTP if he receives it instantly. This wasn’t always the case though, and it’s worth looking at how payments evolved.

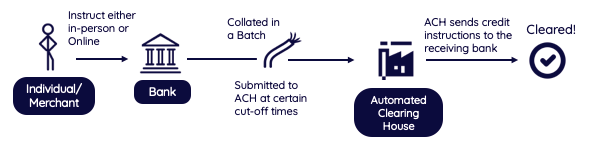

One the humble end of the spectrum we have the basic cheque clearing system. This basically consists of a central party or a “clearing house” that receives and processes instructions. Basically all your cheques are physically moved to a Clearing House who does the accounting – and as we know this takes a couple of days.

This eventually evolved into a more advanced system called ACH or Automated Clearing House where banks would send electronic transactions to the clearing house. The key here is that they were sent in a batch; so a bank would collect all the payment instructions received and send it off to the clearing house electronically at certain pre specified cut-off times. Naturally this is much quicker. So going by the earlier example if you use your phone app to send funds to a friend, and they settle in half a day or a day – it’s almost certainly powered by an ACH system.

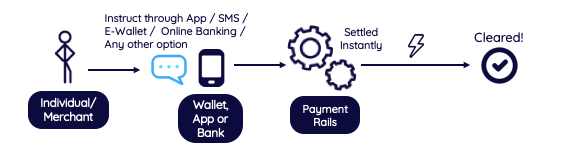

The final evolution has been the implementation of Real-Time Payment Systems. These are simply what the name implies. And this is actually a relatively recent invention. South Korea was the first country to launch one in 2001; the UK’s Faster Payments came online in 2008; the Eurozone’s TARGET RTP (TIPS) went online in 2017 and the US only got its first RTP in 2018. In the US’s case, it’s interesting to note that this is a private initiative by The Clearing House, and the Fed has only recently announced development of its own FedNow system which will only come online in 2023 / 2024.

And it’s important to remember that this is basically just the “plumbing”. As a user you will access RTP via some other third party like your bank’s mobile banking app. If you send money through say HSBC’s mobile app to your friend’s account – in an ACH world this takes up to a day to clear but RTP pushes it through instantly.

India’s PayTM and Kenya’s M-PESA are a good example of services (India has since implemented it’s own RTP) popping up to compensate for the inadequacy of national payment systems. In an ACH and Cheque clearing-driven world, digital wallet services were a good alternative. And M-Pesa was launched way back in 2007 - it built a parallel infrastructure leveraging the capabilities of mobile phone operators. It enabled Kenyans to transfer money to each other through the use of SMSs. AliPay and WeChat the most popular digital wallet apps by far, also started off in a similar vacuum. It’s a testament to their success that China hasn’t bothered with an RTP system.

In an RTP driven world, these apps aren’t entirely revolutionary. Any bank or member of the RTP system can pretty much send payments instantly so while the Venmos, and Wechats are pretty much here to stay, their proprietary infrastructure isn't particularly groundbreaking.

One key distinction that needs to be introduced here is between Large-Value Payment systems and Small value payment systems. Payment systems haven’t exactly been democratic – some of the faster and quicker ones were not accessible to the public. So I lied when I said South Korea had the first RTP in 2001 – in a different form real time payment systems have been available for decades; but only to large Financial Institutions and Corporates. These are typically go by the moniker of Real-Time Gross Settlement systems. Banks and FIs use these for securities settlements, interbank activity and facilitating large clients. These systems are much more secure and offer the complete range of transactions. So RTP systems for security reason disable certain transactions e.g. you are unlikely to be able to use them to buy a house.

So if you’re looking at something US Treasury bond issues or redemption; the process certainly won’t be handled through mail-in checks. If BoA decides to purchase the latest issuance of 10 Year T-notes, the payment will be sent to the Fed instantly via the use of FedWire, which is the US’s Large Value Payment System.

Cross Border Payments

This is where it gets more convoluted. Cross-border payments aren’t really managed via a system per se. So there is no equivalent of an ACH, RTP etc, and basically an International Payment system doesn’t exist. Cross-border Payments are effectively quarterbacked by what is known as the “correspondent banking” system. In easy terms, the correspondent bank network is banks exchanging money with one another. Simply put, if you send money to someone from Singapore to Australia; basically you need one Bank to be ready to decrease its Singapore account balance and increase the one in it's Australian branch. It plays out something like the below.

You would have heard of SWIFT and may be wondering where SWIFT factors into this. And SWIFT is in fact not a payments system but simply a messaging system which facilitates secure and instant communication. Security is really key here, so when SCB Australia receives payment instructions as above via SWIFT, they know they haven’t been duped. SWIFT has a universal monopoly over cross-border payments - and access to SWIFT is one way financial sanctions are implemented. Recent US sanctions against Iran were implemented by causing designated Iranian entities to be removed from the system. Predictably this has lead to online . For kicks, here’s a Russia Today video branding SWIFT a “tool of the US empire”

If you consider the flow the above – it becomes clearer why cross border payments are sometimes costly and time consuming. There are too many handshakes, and SWIFT is not exactly inexpensive. So that's why small value payments tend to be neglected and expensive. This is a problem all too familiar to the millions of low-wage expat laborers from countries like India, Pakistan and the Philippines. A good example of a Fintech that has succeeded in offering a decent solution to common folk is "Wise". Ultimately it’s fundamental structure is built on the back of a correspondent banking network only but they use something called a Peer Currency Exchange model to offset costs, which you can read about here.

As we saw in the case of RTP Systems, however, these problems are not universally shared. Large Financial Institutions and Corporates are able to tackle these problems through bespoke arrangements. If you parse through the organizational structures of banks – a lot of them have departments going by something to effect of “Transaction Banking” or “Treasury Services”. So JP Morgan has a “Treasury and Payments” department, Citi has a “Treasury and Trade Solutions", and BoA has “Global Payments” department. Among other services, they also facilitate access to payment infrastructure systems for large clients. Here is an example of BP Shipping who managed to obtain the services of an MNC bank’s global branch network to manage it’s global payroll. Here’s another example of a bank assisting Alibaba in centralizing it’s Treasury in Singapore. Basically in both cases, the banks are not only providing timely cross-border transfers but also facilitating access to the local ACH, RTP and Large Value Systems. Many of these corporate solutions tend to be bespoke, and that’s natural given the immense underlying complexity. And by their very nature, they are indeed hard to commoditize and scale. Still, I feel there is a missed opportunity here, and global banks could have leveraged their correspondent banking networks to develop a truly global cross-border app. While not lucrative in the short-term, the captive user base would have paid off significantly over the long run.

There have been some attempts by regulators to add a layer of technology to cross-border payments. The EU has introduced SEPA, a sort of real-time system for European countries. China recently come up with cross border payment system called CIPS which would offer efficient clearing and settlement for RMB. In a utopian scenario, the world could potentially move to a single real-time payments system, which would do away with all the layering and complexity. And this really speaks to the promise of Blockchain and other digital assets as they effectively do away with all the layering and complexity. But it’s also easy to see how a unified and improved account-based system without blockchain could potentially deliver the same results.

In the present political climate, these systems can instead potentially become even more closed and nationalized. We mentioned the role of SWIFT in sanctions. Effectively this is done by asking SWIFT to suspend certain parties from the system. And that is one reason why certain countries are keen on digital infrastructure. In 2017, Vladimir Putin had a tete-a-tete with Ethereum founder Vitalik Buterin to discuss “Ethereum” opportunities. This is a rich and speculative topic, but payments are indeed one of the frontlines of the new cold war.

Credit Card Payment Networks

Up till now we didn’t really the role of Card Processors . Despite being burdened by a lot of legacy mumbo jumbo , the proprietary networks maintain by VISA and MasterCard are fairly efficient. One issue with Bitcoin and Blockchain has been scalability – bitcoin can only process around 4.6 transactions per second; VISA can deliver 1700. They are also ubiquitous in online banking and all know through our online shopping experience that cross border payments are no issue.

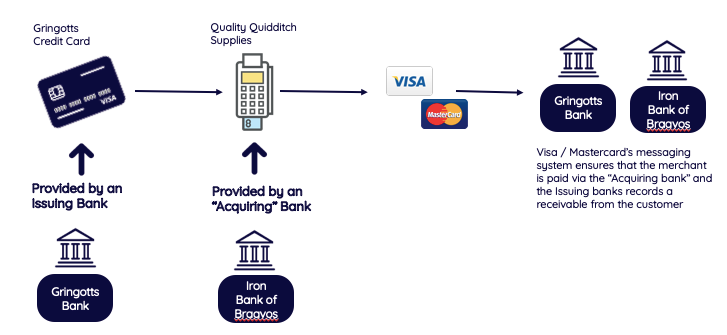

Dee Hock, the founder of VISA and the whole concept of the credit card payment network, has express disappointment at how Credit Cards have become a tool for managing debt rather expediting payments. Looking at their setup, it becomes clearer why. They have an odd incentive scheme for financial institutions called “interchange fee”; and it goes something like this.

Effectively, whenever a purchase is made the “acquirer” (or the bank facilitating the payment through it's merchant terminal) has to pay the “issuer” (the bank funding the card that is swiped); the economic logic here is that the issuer takes on the cost of funding the card and the merchant or acquirer would not have access to the transaction if it weren’t back by the card.

In reality, this logic is slightly contrived. Many card bearers are simply transactors rather than borrowers, and just use the card for making payments. And these days, while people rack up credit card bills it’s hard to imagine life without credit cards. The Interchange network effectively penalizes merchants. This is a good segue to talk about how Merchants have consistently been duped and de-prioritized by large Financial Institutions. In the example above, it quite likely that the merchant ends up bearing the cost of interchange. Anecdotally, I have been in situations where this fee was in fact passed on to the customer and I had to foot the bill by paying ~2% just for the privilege of swiping my card.

In China, credit cards did not take off for this same reason. Merchants did not like being charged money and eventual deployment of the QR Code proved far better. The Merchant opportunity in general has been leveraged very well by Alibaba (by offering escrow to merchant, and then a host of other services), Square (by offering decent payment gateway options), and Stripe (by offering fantastically detailed APIs) to build their massive user bases.

So what has Fintech done ...

Fintech has tried to optimize many of the issues confronted by individual and institutions. There continues to be a lot of venture capital thrown there. According to Pitchbook, ~ $17Bn was raised by Paytech firms and digital assets in Q3’20 alone; and this accounted for nearly a third of all Fintech capital raised.

A good example of Payments innovation use has been “Wise”, which we discussed above. The other standout cases have been in the digital Wallet Space (WeChat, AliPay) or e-commerce (Square and Stripe). What’s interesting to note is, and this may not be obvious to the layman, that real tangible change only been driven by a few players viz. regulators (through development of real-time payment systems and “open banking”), the blockchain ecosystem, and a handful of startups.

Take the case of Revolut, for instance. Their much-hyped card has become a popular consumer product and – and while certainly good service it’s basically a card on VISA with less frills. In that regard, much of the hype around Fintech in the payments space is just that.

Brave New World

Having looked at the complexity underlying, payments it become obvious why Bitcoin and Blockchain technology in general have generated so much excitement. As you almost certainly know by now, there are no hand shake and no intermediaries involved. Ease, anonymity and seamlessness are unparalleled. On the flip side, scalability has been a huge issue. It is not easy to see how something like Bitcoin can handle the sheer volume of global payments especially when the existing infrastructure already consumes 0.6% of Global Electricity (!).

Bitcoin and crypto in general is a rich topic and there is a plethora of resource out there that cover the topic better than I can. One of the best and objective treatments I have seen on the topic is the excellent Citi GPS report on the future of money which you can access here. We will brief discuss CBDCs, and China’s efforts to develop one in particular which is a nice way to round out the themes we have been discussing.

CBDCs once implemented are most likely to eventually void the whole panoply of payment infrastructure that we have been discussing. In terms of development, China is the leader here with its DCEP (Digital Currency Electronic Payment) initiative already having undergone some pilot tests. Other countries are racing along though, and the BIS has an excellent overview of global efforts to develop CBDCs. As a side note, it’s worth noting that DCEP does not use blockchain technology though it does make use of asymmetric cryptography. It is also centralized with the PBOC operating a “registration center” to manage the ledger and records.

One of the most fascinating aspects of is that CBDCs are highly likely to disintermediate banks. If you are able to deposit fiat money in a digital wallet there is really no need for Banks to act as depositary agents. But without this function, it is unlikely the banks can shore up liquidity for any of their activities. Of course it’s unlikely that governments roll out CBDCs wholesale and risk the whole financial system.

Having said that, CBDCs may get there piecemeal. China’s DCEP works by issuing digital coin to banks who can then let customers swap their deposits for currency. But this may not be the design for other countries. Digital Currency can directly be issued by Central

Given the potential disruption to the financial system, why are governments interested in CBDCs? For one thing superior digital records will enable targeted and precise monetary and fiscal policies. The entire edifice of modern economic management is broad-based management built on statistical models. CBDCs can potentially enable a “Big-data”esque approach with micro-targeting of individuals for fiscal and monetary incentives. Embedding smart contracts in the currency can potentially also link interest payouts to variables like statistical information such as GDP, Inflation etc. If you think of it this way, CBDCs will profoundly impact societies like no other invention before.

Going back to the China’s DCEP – one application of great interest to Chinese regulators are cross-border payments. As of now, the overwhelming majority of Chinese trade is denominated in currencies other than they yuan. Historically, China has had a longstanding policy of not allowing exchange convertibility for the renminbi. This policy allowed it to manage the renminbi and keep it relatively undervalued to boost its exports. But now that China dominates international trade, it can reap the benefits of a strong global currency. It started efforts to Internationalize the RMB nearly a decade ago but progress has so far been slow. A Digital RMB that simplifies cross-border payments can provide a huge boost to this initiative. With US-China trade tensions, currency independence becomes all the mort important.

Thanks for reading! I hope I’ve managed to convey how profound some of these developments are, and how widely society at large may be impacted

Bibliography: (🎙 / 📺 / 📚/ 🧑🏻💻)

The Citi GPS report on the Future of Money is one of my favorite resources on the subject

“Global Payment Reports” by Carol Coye Benson is a great read on the technical nuances of Payment systems

“Beyond Blockchain” by Erik Townsend is a great gonzo-esque discussion on the geopolitical aspects of blockchain and currency

….while Eswar Prasad’s “The Dollar Trap” is a more genteel, scholarly treatment of the same subject

Faisal Khan’s Youtube Channel is an excellent dossier on technical payment subject