The Rise of the Renminbi 🧧

And Hong Kong’s Role as an Offshore RMB Hub

Hi Folks 👋

Sharing a wonkish piece I wrote for “The China Guys”. While I’m reproducing the article below, I would strongly encourage you to head over to their website and view it in it’s original glory here (<<🔗 ).

“The China Guys” are really one of the cooler outfits operating in the somewhat crowded China policy and advisory space. Their writings are some of the most incisive and respectful pieces on China’s development. Their website has tones of cool content, and they also run an awesome newsletter. My article is part of their Rise of the Renminbi series and if you are interested in an introductory guide to the topic you should first check out Nathan’s excellent piece here (<<🔗 ).

Now, the headline likely sounds dry and obscure but let me give you some context into why its anything but. The Renminbi’s rise is one of the most fascinating macroeconomic journeys of our time. We all know China as the world’s most dominant trade player. What folks unfamiliar don’t realize is , virtually all of their trade is denominated not in the Yuan but the US Dollar.

Historically, this has been a conscious choice by Chinese policymakers for developmental. However as China’s role has grown, it has felt the need to pivot and internationalize its currency. Japan faced a similar choice in the 80s when it dominated international trade but the Yen stayed (and to a great degree still is) a domestic currency.

Diving into this topic also gives one a glimpse into some of the linchpins of the global financial system. Much of the current status quo stems from the post-WW2 Bretton Woods Agreement. This is a rich topic but suffice it to say, this was when US Dollar was first conferred it’s so-called “Exorbitant Privilege”; an outsize role in the global financial system.

Currency economics is a topic I’ve generally become interested in - and I plan to write a bit more in the coming days. I am going through Benn Steil’s excellent “The Battle of Bretton Woods”, which talks about Keynes’ fight to ensure a more representative global order post-WW2. Interesting these themes are quite popular in crypto circles. It’s not uncommon to find Bitcoin and Blockchain enthusiasts almost conspiratorially railing against the financial order. One cryptocurrency is aptly named “Bancor” after Keyne’s proposal of a supranational currency.

I also cover the topic vis-a-vis Hong Kong’s role. And this lens allows me to look at what it takes to build and sustain a financial center. Having lived and worked in two global financial centers, I have had a keen interest in the policy choices that led to the extraordinary success of cities like Singapore, London, Dubai and of course Hong Kong.

*******Article text begins*****

Summary

A global RMB is a strategic long-term policy goal for China, and a deep offshore market is a crucial prerequisite. As a key offshore RMB hub, Hong Kong will have to embrace supportive policy and build financial market infrastructure to bolster the RMB’s internationalization. This article takes a look at the potential levers available to both Hong Kong and Mainland authorities to advance this agenda.

It is well known that until 2009, virtually none of China’s external trade was denominated in the Chinese yuan. There was no circulation of the renminbi (RMB) outside of the country, and no lawful way to channel the RMB back to the Mainland via the banking system. Limited capital and current account convertibility has been a conscious choice for Chinese policymakers because an underweight yuan has historically been a key driver of their export-led growth strategy.

However, as China has come to dominate international trade, Beijing has become more interested in the strategic benefits of a widely traded currency. RMB internationalization was first articulated in the 12th five-year plan (FYP) as a strategic priority, and consistently reaffirmed in the 13th and 14th FYP. Hong Kong was selected as a key locale for RMB internationalization, and the creation and controlled development of the city’s offshore RMB market was part of China’s first step in its campaign. Boosting Hong Kong’s role as an offshore RMB center was also highlighted in 2019’s Greater Bay Area Developmental Outline, offering insight into Beijing’s future ambitions to continue advancing its internationalization agenda through the city.

Crossing the River by Feeling the Stones

A deep and vibrant offshore market is essential to internationalizing the RMB. In this context, an offshore market simply refers to a pool of readily available RMB outside of Mainland Chinese borders. The US dollar, for instance, is widely available outside of its home country, which has been a natural function of its dominance in the post-WWII era.

The considerable supply of dollars outside US borders is referred to as the “Eurodollar Market.” The supply of “Eurodollars” is estimated to be in the ballpark of US$14 trillion as of 2016. To put that into perspective, the US’ domestic money supply (M2) totals around US$19.6 trillion. So, the international supply of dollars equates to nearly 71% of domestic liquidity. China’s RMB, by contrast, is not currently widely available outside of the Mainland. Based on data from the St. Louis Fed and Global Capital, total offshore RMB deposits are a mere 0.55% of China’s domestic M2 money supply – a consequence of China’s closed exchange rate policies. Historically, most external trade was settled and invoiced in US dollars, with the RMB primarily used for domestic transactions.

Even if the doors to RMB convertibility were immediately opened, multinationals, financial institutions, and international players would be reluctant to transact without sufficient offshore venues to park funds and options to manage risk. One of China’s biggest imports is iron ore, the majority of which comes from Australia. For Australian companies like Rio Tinto and BHP Bilton to be comfortable with receiving RMB as payment, they would need the means to be able to invest these funds and convert them to AUD for their own domestic purposes. They would also need to be able to hedge exchange rate volatility through the use of derivatives. All of this requires a large supply of RMB in the Australian financial system, which there currently is not. As a testament to the RMB’s historic illiquidity,the first yuan-based iron ore sale was only completed in 2020!

While there has been significant RMB liberalization over the past few years, much remains to be done. The RMB’s share in trade settlement stands at 2.2% of world trade, which is in stark contrast to its global export share of 13%. Much like China’s broader 20th century reform, gradualism has been the hallmark here, and Deng’s maxim of “Crossing the river by feeling the stones” is apt. Case in point, the Hong Kong offshore market has been used to allow China to cautiously liberalize its currency in a controlled fashion without completely opening the Mainland’s capital account.

Hong Kong’s Unique Role

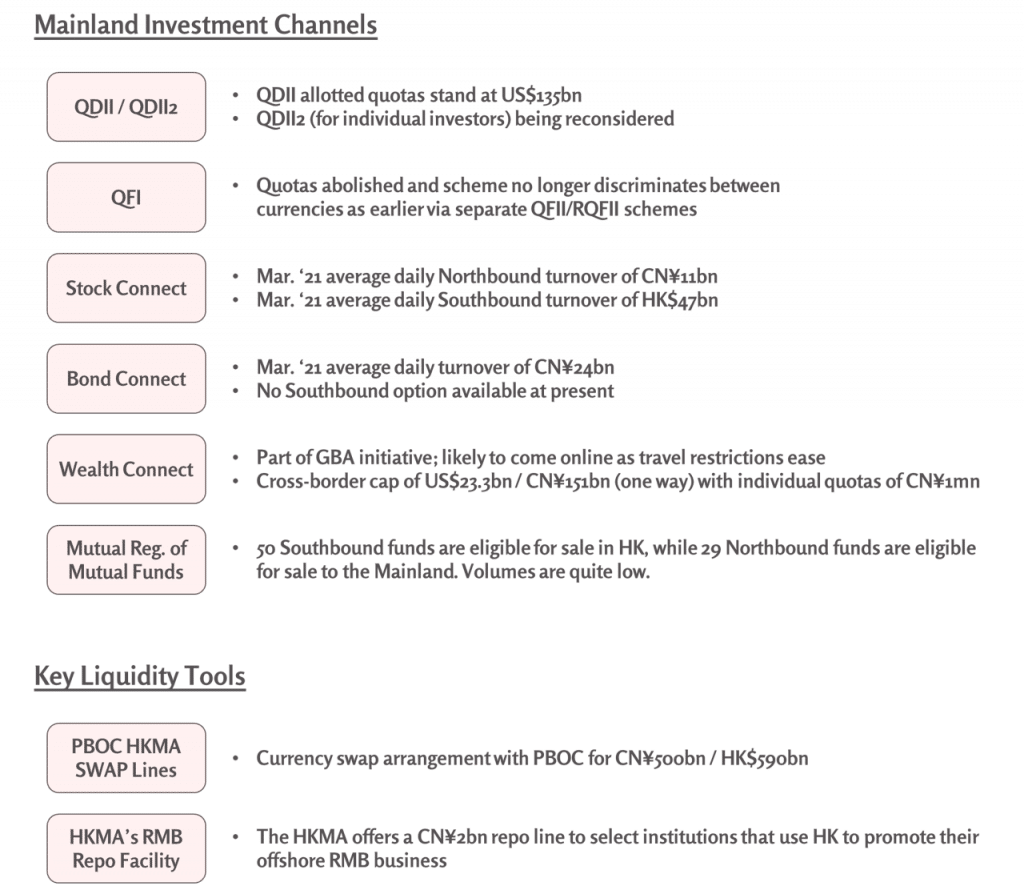

China’s internationalization efforts really took off in 2010 when it established the Hong Kong Offshore Market. This allowed select banks to conduct RMB business and established a swap line and memorandum of understanding with the Mainland’s central bank, the PBOC. Despite other major financial centers like London and Singapore, both of which have a share of the offshore pie, Hong Kong remains in the leading position. At present, Hong Kong facilitates 75% of all RMB offshore payments and commands CN¥761 billion of RMB deposits, which is approximately half of the global total.

This position truly is an extension of the city’s natural role as a bridge between the Mainland and the rest of the world. As a financial center, it exercises a monopoly over key investment channels into China. The RMB’s internationalization and Hong Kong’s growth prospects coexist, in large part, on expanding these channels to support greater RMB flow.

Primary Investment Channels

In addition to its mandated role, Hong Kong excels in terms of financial market infrastructure and offers the largest number of listed RMB derivative products (currently numbered at 15 products. The Singapore Exchange is in second place with eight). While the expansion of these investment channels would be subject to broader considerations like market demand and prerequisite infrastructure, further product enrichment and diversification can strengthen Hong Kong’s role as a preferred booking center for financial institutions and investors, alike.

Building Upon Hong Kong’s Position

As China’s relentless growth story and political headwinds pivot Hong Kong towards the Mainland, a superior RMB offering will become key to its competitive positioning. Both the HKMA and Hong Kong Exchange (HKEX) have been actively promoting the offshore RMB market in the city. Mainland authorities have also offered a host of policy suggestions in their May 2020 circular “Guiding Opinions on Supporting the Financial Development of Guangdong-Hong Kong-Macao Greater Bay Area.”

Leveraging and Developing “Dual Counter” Options

The HKEX was the first exchange in the world to offer a “Dual Tranche Dual Counter” option for RMB listed securities. Effectively, a Dual Counter allows issuers to raise funds in both HKD and RMB. Both classes of shares are equal, and shareholders may subsequently transfer their shares from one counter to another.

In the equities space, this area is still woefully underdeveloped, with only one company (Shenzhen Investment Holdings Bay Area Development Company Limited) utilizing this option. Exchange-traded funds (ETFs) fare better, and several listings have RMB counters. Popular ETFs like the S&P SPDR 500 and various gold ETFs have RMB counters and could be of further interest to retail investors. There are also RMB-traded commodity derivative options available as well as a singular REIT listing.

Dual Counter usage could potentially grow with the emergence of QDII2, the China- Hong Kong ETF Connect, and the Wealth Connect, all of which will empower Mainland investors to invest abroad. This will bode well for yuan utilization, as Mainland investors will prefer to invest in RMB overseas to avoid exchange rate risk.

RMB Bond Market Development

Hong Kong has long been the preferred destination for issuance of the so-called “Dim Sum” bonds. Dim Sum bonds are RMB-denominated bonds issued offshore, and this pool of RMB assets currently stands at CN¥658 billion. Bond Connect trading volumes account for 53% of China Interbank Bond Market (CIBM) trading value, suggesting this is a fruitful area.

Regardless, there still remains significant runway for development as the bond market in its current form lacks depth. Potential areas of focus could be: (a) developing RMB bond futures and options, which at present are non-existent; (b) opening up Hong Kong market access to Mainland traders through the Bond Connect; (c) developing an efficient repo market which does not really exist at the moment either.

Integration into the Greater Bay Area

One of China’s key focus areas is the Greater Bay Area (“GBA”) Development Plan, which will naturally be a huge source of RMB activity in and out of Hong Kong. An outline of how regulators expect financial markets to develop gives several special mentions to increased cross-border usage of the RMB, with a strong emphasis on the city’s role in facilitating this.

One of the most important themes in the Greater Bay Area Development Plan is better financial integration of the GBA. GBA-based banks will be allowed to conduct cross-border RMB lending, engage in RMB derivatives, and also cross-sell investment products. At present, from a regulatory perspective, there is no difference if a Mainland client of a Hong Kong bank hails from Guangzhou or Shanghai, but this looks set to change as Hong Kong and Macau-based banks are increasingly encouraged to expand their footprint in the wider GBA.

There is also a nod towards encouraging investment in domestic private equity funds and venture capital funds in the GBA through the use of a “qualified overseas limited partnership” channel. This is expected to take place through expanded use of the QDIE channel. Foreign investors will be encouraged to establish foreign-controlled securities, fund management and futures companies, and life insurance agencies in the GBA.

Finally, the rollout of Wealth Connect will enable ~64 million GBA residents to invest in wealth management products. Note that relative to other schemes, the total dollar cap is slightly smaller at ~US$45 billion. The scheme’s launch has been hamstrung due to the pandemic, as participating in Wealth Connect requires in-person account-opening for compliance reasons.

Potential Uses of the Digital RMB for Trade Settlement

China’s CBDC development efforts have received significant coverage, and it will likely be the first major economy to launch a fiat-pegged digital currency. One of the most significant use cases for a CBDC is trade and cross-border settlement. Hong Kong has already participated in the e-CNY pilot program. As the largest offshore center, Hong Kong could potentially take a leading role in its eventual wider deployment.

Potential Challenges (and Challengers)

At this point, it is worth noting that there exists a bit of a chicken-and-egg dilemma. On one hand, there is much that regulators, exchanges, and market participants can do to advance the offshore RMB market. But ultimately, the success of these policies hinges on demand and supply of the currency itself, and a larger RMB pie can only come about through the process of market liberalization.

Having dual counters for REITs, for instance, would not lead to much if offshore investors are not terribly interested in Mainland REITs. By the same token, if Mainland issuers are able to secure RMB funding onshore without significant hurdles, then there is little incentive for them to list offshore. This part of the equation can only be solved by greater current and capital account convertibility. Further expansion of cross-border trade under schemes like QDII2, Wealth Connect, and the GBA Development Plan will, by their very nature, deepen the offshore RMB pool. Some natural developments like China’s imminent addition to the FTSE Russell World Government Bond Index will also nudge things along.

There is much more to parse out in the details of China’s investment channels as well, and granular reform could also unlock value. QFI, for instance, until recently, did not allow for listed futures and options as part of the quota. To take another example, foreign investors are not allowed to own more than 10% of the shareholdings of a listed company.

While progress seems glacial at times, Beijing has been consistently rolling out incremental and meaningful liberalizations. A detailed timeline of RMB policy changes is present in the 2020 RMB Internationalization Report, which is firm evidence that steady progress continues to be made on a regular basis.

Other financial centers have also been keen to attract RMB-related business and have done much in the way of infrastructure development. A lot of this is not really a repudiation of Hong Kong, rather is simply a natural response for other jurisdictions to roll out their own iterations.

London

Outside of Greater China, London is the leading offshore RMB center and actually leads Hong Kong in RMB FX Spot Transactions per SWIFT (though it is much smaller on an aggregate basis). London is, by and large, the world’s largest FX hub and the City of London Corporation has worked to develop the offshore RMB business as a natural extension of London’s standing.

As a trading center, London’s time zone allows it to provide liquidity after the markets in Hong Kong and the Mainland have closed. London also has an active Dim Sum bond market (CN¥45 billion as of July 2020) and a nascent stock connect scheme with Shanghai (with four listings so far).

Singapore

Singapore is already Asia’s largest FX Hub (ranked third globally) with connectivity to ASEAN, and by some measures, a hair’s breadth away from London as an offshore RMB hub. It is also expanding greatly as a wealth hub – a trend which could continue given Hong Kong’s diminishing international prestige.

Given Hong Kong’s monopoly on investment channels, it is unlikely that Singapore will take serious market share away, but it can target different segments of the offshore pie. It is preeminent as a corporate treasury center and has deep liquidity in Asian currencies (which are not necessarily restricted to ASEAN; as an example, Indian rupee derivatives are exchange traded on SGX). One corollary of all this could be a stronger cross-currency game for Singapore.

Taipei

Taiwan commands the second-largest offshore RMB deposit base on account of being China’s largest import partner. Much like the Mainland, it is exchange-regulated with the New Taiwan dollar being restricted and not widely available outside of the country. The regulatory regime is strict, and Taiwanese financial institutions can only transact in foreign currencies through the use of “Offshore Banking Units” (RMB usage has been, however, extended to “Domestic Banking Units”).

Despite the large trade in RMB, its macro inflexibility and recent political developments imply that Taiwan is unlikely to emerge as a significant offshore RMB center. However, there is potential for targeted development given Taiwan’s significant national savings. These savings, coupled with low interest rates, have led Taiwan’s export-rich corporations and insurers to seek returns in the form of the so-called “Formosa” bond market – which counts Apple, Verizon, AT&T, and Qatar National Banks as issuers. While largely USD-based, the RMB Formosa market continues to flourish as well.

Other Players

The Deployment of OBOR will, by design, necessitate mini-hubs. China already has the largest number of Central Bank Bilateral Swap Arrangements (35 agreements vs the US’ 14) of any country globally with a potential US$500 billion equivalent of RMB firepower on standby. As a consequence, other financial centers will develop some degree of RMB self-sufficiency. Many German financial institutions have begun participating in the RMB business given the country’s strong export orientation. Luxembourg, too, is leveraging its status as a center for fund management. In the Middle East, the UAE is gearing up similarly and has RMB clearing arrangements in place; its largest bank, First Abu Dhabi Bank, issued a small tranche of RMB bonds in 2019.

Looking Forward

China has traveled a long way in terms of liberalizing its markets during the last decade, and looks poised to continue progressing forward. Its “Long March” towards RMB internationalization is a complex enterprise that dovetails with many of the country’s strategic pursuits, including the Belt and Road Initiative and the Greater Bay Area scheme. Hong Kong’s differentiating edge as a financial center will be molded by these developments and will find a rewarding trajectory should it continue to build on its superior infrastructure.