PayTM and the battle for India’s Ecosystem

PayTM’s upcoming IPO will set the stage for one of the world's most definitive ecosystem battles, with Big Tech, China Tech and local champions duking it out.

Welcome to The Macro Geek, where I write on themes in business, finance and technology. If you haven’t done so already, please hit subscribe 🙏

Hey Folks 👋

PayTM’s upcoming IPO is set to be India’s largest yet. Already a harbinger of greater investor enthusiasm, I believe the stage is set for one of the most definitive ecosystem battles to play out in India and one with likely global ramifications. A great chunk of PayTM’s prospectus tries to sell you on the idea that the India of now is the China of circa 2010, and does a fairly convincing job.

More interestingly apart from local champions like PayTM and Reliance, you have significant Big Tech involvement as well. And the country is becoming sort of a field experiment for some of their larger plays. Case in point: India is one of the few countries where WhatsApp Pay and Google Pay operate. In the eCommerce space, Amazon competes neck and neck with Walmart-backed FlipKart. PayTM itself has significant backing from Jack Ma. Other Chinese tech titans like Tencent and Meituan are variously invested. Pinduoduo-style social commerce is also emerging in form of companies like Meesho.

PayTM’s story is also a good segue into a wider look at India’s trajectory. Having cut its teeth as a digital wallet, it’s betting the house on branching off into eCommerce and financial services.

It’s worth noting that while India trails China in terms of GDP, its demographics (a median age of 28 years vs 38 for China) suggest much more headway. And China looms large in PayTM’s story, both with regards to its origins and in how it’s trying to develop wider ecosystem. Alibaba was one of PayTM’s earliest investors, and founder Vijay Shekhar Sharma is an obvious Jack Ma fanboy..

I talked about the taxonomy behind payment systems in an earlier article. PayTM started off similar to M-Pesa as a “layered payment solution”; a proprietary wallet superimposed on age old clearing-house infrastructure. PayTM was one of the first to allow for convenient P2P digital transfers.

India has since upgraded its national infrastructure to a Real-time Payments System (“Unified Payments Infrastructure” or UPI), lowering the barriers to entry for other participants. And PayTM was actually slow on the the uptake here - it moved to UPI much later than its rivals. On account of that and despite its namesake, PayTM is actually less about payments than you may think. According to the latest UPI data payments are dominated by PhonePe and GooglePay with PayTM a distant third.

Nonetheless, it has survived all these transformations fairly well. There is a fantastic article by Marc Rubinstein on PayTM’s capacity for reinvention, which was really essential for its survival given the tectonics shifts in India’s Payments landscape. Here is a succinct summary:

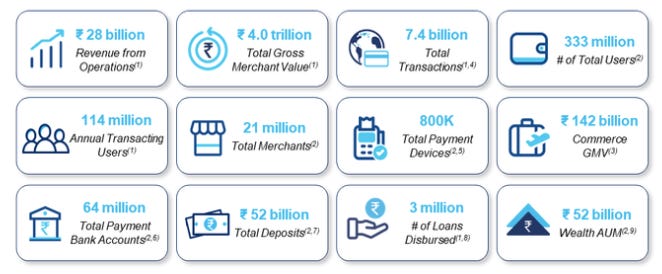

While it’s dropped off in the payments space, it still remains popular as a digital wallet. It’s MAU of 333mn compare favorably to WhatsApp’s (a near universal app in India) 390mn.

One of PayTM’s strongest moats are the nearly 21 million merchants it has onboarded. It’s been very much focused on what Square’s Investor Relation team dubs “the seller ecosystem”. Globally merchants have been one of the most underserved segments of our conventional banking system. And here we see Vijay Shekhar drawing inspiration from Jack Ma.

The story of digital payments in China is well known but is worth repeating. When growth in China started taking off, there was massive resistance to credit cards due to the significant merchant charges levied by acquiring banks. Enter the now ubiquitous QR Code. A decidedly cheaper technology – which does not of need a card acquiring machine and 24/7 online connectivity. Merchants can instead just prop up a QR Code print-out. They don’t even need to be online so long as the customer’s phone has data connectivity. WeChat and AliPay introduced proprietary versions of their QR Codes in 2011 and 2016 respectively. Interchange costs were a huge factor in QR Code Adoption as well - WeChat & Alipay charged a mere 1.6% vs 3% of credit card acquirers.

PayTM did much the same in India – introducing merchant QR Codes in the country for the first time. It’s worth noting India is home to almost 63 million MSMEs (Micro or Small Medium Enterprises). Think “Kiryana” or mom-and-pop stores.

So how is PayTM leveraging this base and building its ecosystem in general? To say that Mr. Sharma is going the whole hog is really an understatement. PayTM’s IPO prospectus references everything from the VC lexicon. You have aspirations for Buy-now-pay-later (“PayTM Postpaid”), mentioned, Airlines Tickets, and gaming (a PayTM Fantasy Cricket league). You have references to retail investor participation (3%) in the stock market being the lowest in Asia, suggesting Robin Hood-esque brokerage services. You have PayTM Business Payment which provide merchants with Strip style dashboards, and even a modest cloud computing division. You also have references to Gold ETFs and Gold Bonds (Gold being India’s preferred saving vehicle).

In fact, PayTM’s SuperApp ambitions make Meituan’s 36 icon home screen look paltry by comparison. Paramount among these, as far as I gather, is their play for Wealth Management and general eCommerce fare via PayTM mall.

Predictably, revenue and margin disclosures aren’t robust enough to do a deep-dive on these segments. And the absolute dollar here is obviously less eye watering than some of PayTM’s Chinese and East Asian counterparts, but that’s really a function of India’s lower per capita income and purchasing power. It’s GMV though compares favorably to even pure play eCommerce rivals Flipkart and Amazon India. Official figures aren’t available but per this article courtesy of RedSeer, Flipkart did around $5bn / a month in peak shopping season. Just run-rating that gets you $60bn which is in the ballpark really.

Cohort economics are strong as well and their 5-Year multiple exceeds even Alibaba’s.

The below table is perhaps more indicative of PayTM’s endgame and overall investor positioning. It’s very much billing itself as a bet on India.

Big tech in India: Watch this space

Having given up on China, India is pretty much the largest potential market for Silicon Valley. While Big Tech has done a fairly phenomenal job of monetizing their user base, it has largely accomplished this through advertising. Asia tech has been far more entrepreneurial in this respect, having pivoting into multiple businesses and that’s a fact not lost on their American counterparts.

What’s interesting to note is that India seems to becoming a sandbox for Big Tech’s larger ambitions. Here we have many developments underway with potential global implications.

India is the one of the handful of markets where WhatsApp Pay operates (Believe Brazil saw a release in May 2021). It has been a long road to get there, and it is believed that Facebook’s 10% investment in Reliance Jio was the fillip for Mukesh Ambani to clear regulatory hurdles. Its penetration remains fairly modest at the moment. Presently, it is working on integrating with Jio Retail, and leveraging India’s massive base of Kiryana (or mom-and-pop) enterprises. WhatsApp’s globality can play in its favor as well should it manage to crack the remittance business (there are an estimated 32 Million non-resident Indians). And with Facebook’s crypto effort “Diem” having been rebranded as a relatively non-threatening USD Stablecoin – India and specifically WhatsApp India could potentially prove to be a lucrative pilot market for Facebook’s Diem ambitions.

India is also one of Google Pay’s only successful markets. While Google Pay claims 40 countries, I believe those are largely token offerings in name only. India and the US are perhaps the only markets where it has anything resembling a reasonable product suite. Google Pay did a massive relaunch in late 2020 to position itself as a coherent financial services app. It had signaled its intentions to cross-sell bank accounts in the US under its “Plex” banner. Details are scarce but it may surprise folk to know that it is already launching a bank account offering in India. With 36% Market share in Payments, the Bloomberg article cited does not mince words on what this could presage for traditional institutions. It has also made its first moves towards leveraging its globality by partnering with Wise to offer remittance services across the US, India and Singapore.

And that’s all I have. Thank you for reading! 🙏